An Economic Study of Nayarit's Development Sector: The Intrinsic Need For Market Positioning

This paper examines the economic expansion of the state of Nayarit, Mexico, with a primary focus on coastal development in the housing and commercial real estate sectors. The analysis also considers supporting industries that underpin and sustain recent growth trends, as well as the competitive dynamics shaping development outcomes across the region. The case study spans a range of actors, from multinational corporate developers to locally anchored firms, to assess how strategic positioning influences market dominance in emerging coastal economies.

Within the Mexican economy, a macroeconomic shift has emerged along Nayarit’s Pacific coastline. Public investment by federal and state governments, alongside foreign direct investment, has contributed to increased capital inflows into infrastructure, construction, and real estate development. The expansion of public works and transport infrastructure has improved regional connectivity and lowered barriers to development, while policy adjustments—including changes to zoning frameworks along the coastline—have facilitated new forms of commercial and mixed-use activity.

Together, these dynamics reflect a gradual transition away from a solely tourism-centric growth model toward a more diversified development structure. While tourism remains a central driver of demand, its interaction with real estate, commerce, and infrastructure investment has generated new development patterns not previously observed along Mexico’s central Pacific coast. This paper evaluates the economic implications of this transition through a multi-layered analysis of macroeconomic conditions, local market dynamics, institutional constraints, and firm-level strategies.

This paper examines the economic expansion of the state of Nayarit, Mexico, with a primary focus on coastal development in the housing and commercial real estate sectors. The analysis also considers supporting industries that underpin and sustain recent growth trends, as well as the competitive dynamics shaping development outcomes across the region. The case study spans a range of actors, from multinational corporate developers to locally anchored firms, to assess how strategic positioning influences market dominance in emerging coastal economies.

Within the Mexican economy, a macroeconomic shift has emerged along Nayarit’s Pacific coastline. Public investment by federal and state governments, alongside foreign direct investment, has contributed to increased capital inflows into infrastructure, construction, and real estate development. The expansion of public works and transport infrastructure has improved regional connectivity and lowered barriers to development, while policy adjustments—including changes to zoning frameworks along the coastline—have facilitated new forms of commercial and mixed-use activity.

Together, these dynamics reflect a gradual transition away from a solely tourism-centric growth model toward a more diversified development structure. While tourism remains a central driver of demand, its interaction with real estate, commerce, and infrastructure investment has generated new development patterns not previously observed along Mexico’s central Pacific coast. This paper evaluates the economic implications of this transition through a multi-layered analysis of macroeconomic conditions, local market dynamics, institutional constraints, and firm-level strategies.

I: Macroeconomic Analysis

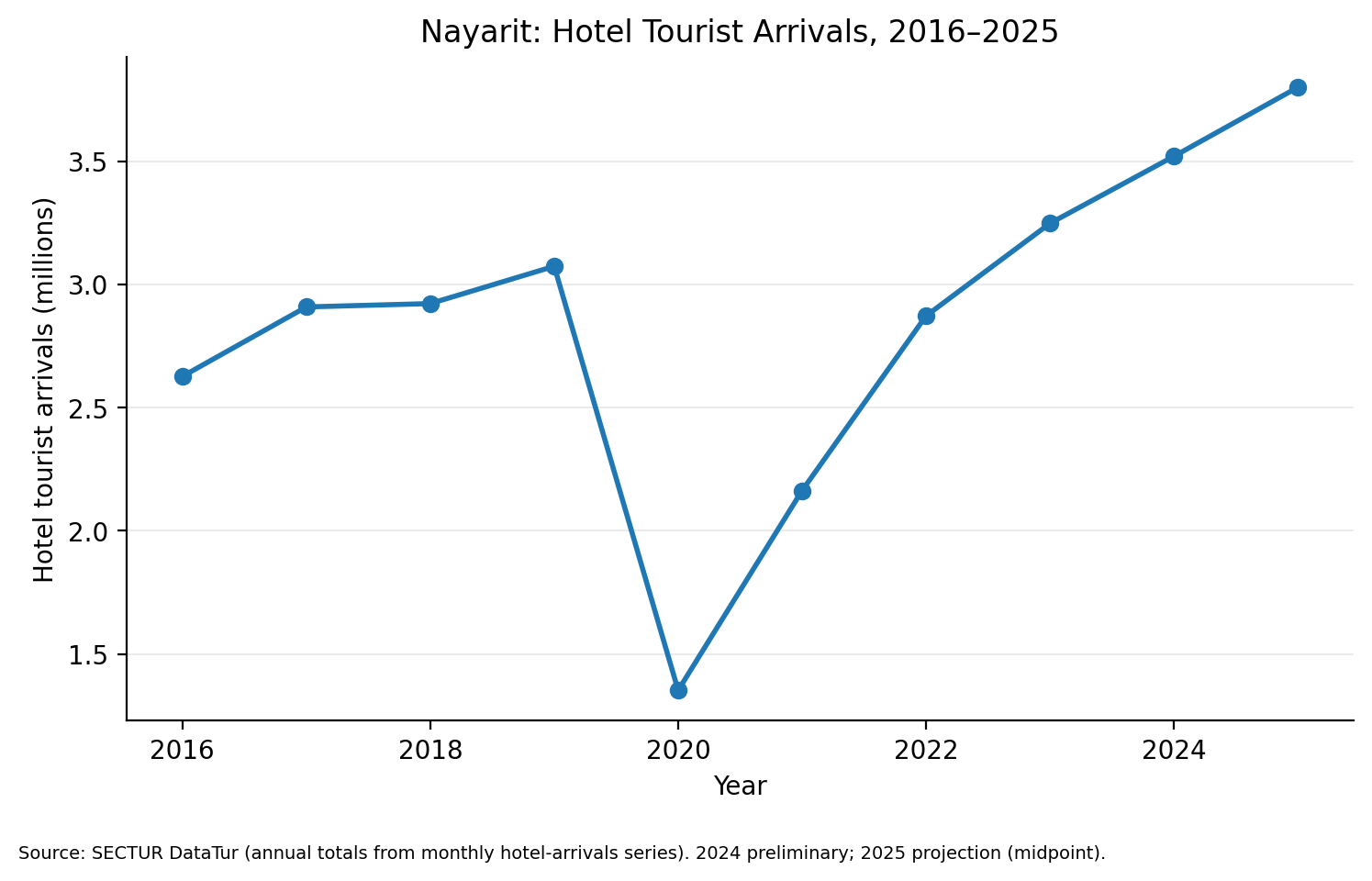

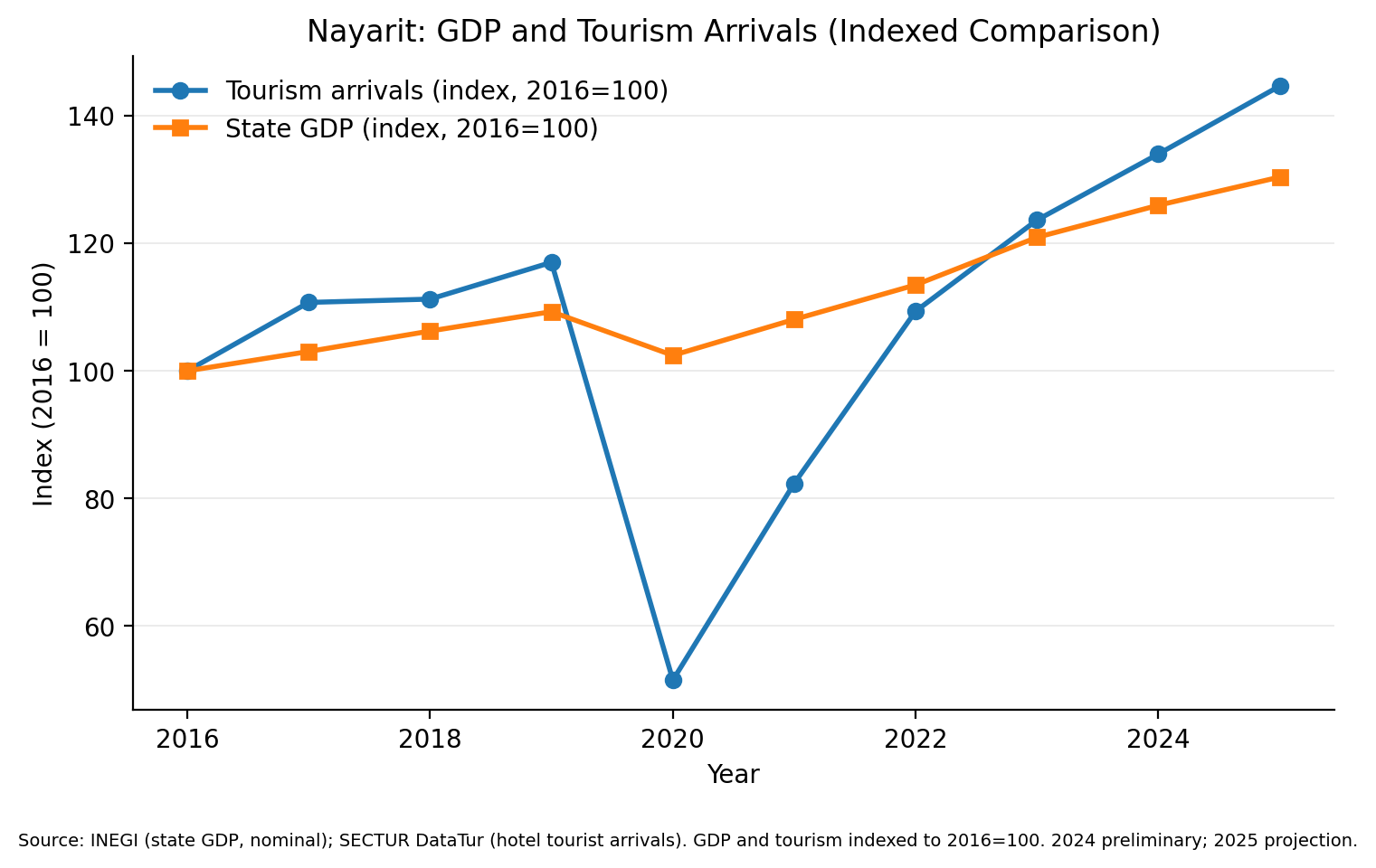

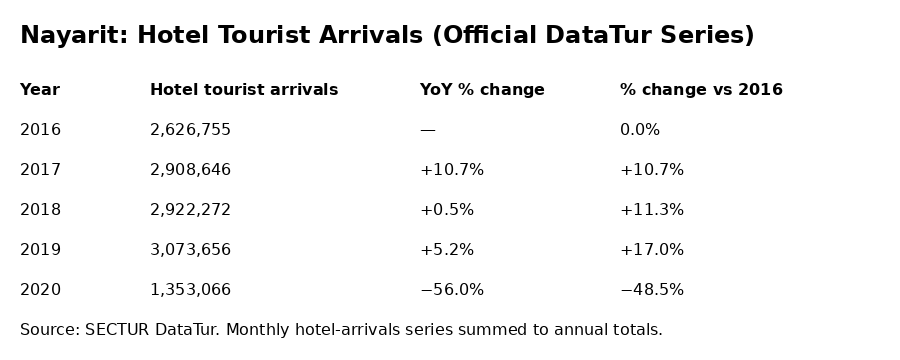

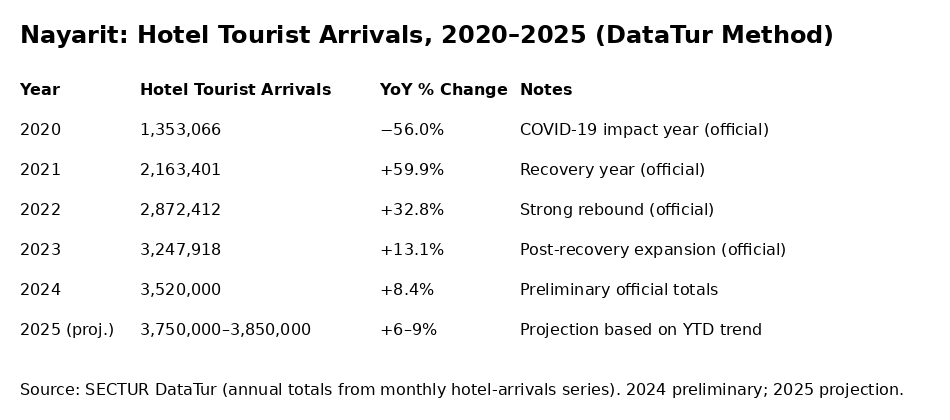

Over the past decade, Nayarit has undertaken substantial public infrastructure investment, estimated at USD 1.7–2.3 billion using period-average exchange rates.¹ Infrastructure spending executed in 2025 is estimated to account for approximately 8–13 percent of total decade-long public investment, reflecting the back-loaded execution profile of large transport and airport projects.² In aggregate, staff estimates suggest that roughly one-tenth of total public infrastructure investment over the past decade was executed in that year. This investment includes the expansion and modernization of statewide highway systems, improving cross-state transportation, commercial connectivity, and access to emerging development zones.¹ Enhanced highway connectivity has facilitated broader economic integration with neighboring states, most notably Jalisco, whose nominal GDP is estimated at USD 129–136 billion based on 2023 exchange-rate conversions.³ The scale of Jalisco’s economy has contributed materially to demand spillovers into Nayarit, including middle- and upper-middle-income households investing in rental properties, vacation homes, and coastal land acquisitions. According to estimates based on household income survey distributions, approximately 61 percent of residents in the Guadalajara metropolitan area are classified as middle-income, with an estimated 18–22 percent falling within the upper-middle-income segment.⁴ These proportions exceed national averages and those reported for the state of Jalisco overall, where approximately 53.6 percent of households fall into the middle-income category.⁴ Within this context, Puerto Vallarta represents the dominant tourism hub in Jalisco. Tourism is estimated to account for approximately 8 percent of the state’s GDP, with Puerto Vallarta capturing more than half of tourism-generated economic activity. ⁵ Author calculations suggest this corresponds to approximately USD 2.22–2.35 billion in annual tourism-related output attributable to the destination. ⁵ Public investment in highway infrastructure has also supported the expansion of air transportation capacity within and adjacent to Nayarit. In the case of Tepic–Riviera Nayarit International Airport, completed modernization works—including runway rehabilitation, a new control tower, terminal upgrades, aprons, and access roads—have been reported at more than USD $146 million, corresponding to executed initial phases of the project.⁶ The broader expansion program is reported at approximately MXN 4.1 billion (USD $223–239 million) under a public–private investment model implemented over the 2023–2027 period.⁷ Complementing in-state investments, neighboring states have also expanded air transport capacity. At Puerto Vallarta International Airport, construction of a new passenger terminal is underway to alleviate congestion and accommodate rising demand. The project represents an investment of approximately USD 490 million and is being executed by Grupo Aeroportuario NAYARIT DEVELOPMENT SECTOR del Pacífico (GAP).⁸ As of 2025, construction progress is reported at approximately 54 percent, with completion targeted for mid-2027.⁸ Tourism demand across Nayarit has increased steadily over the past decade, with temporary contraction during the COVID-19 period followed by a rapid recovery.⁹ Statewide hotel-arrival data from SECTUR DataTur illustrate both the pandemic shock and subsequent rebound, while indicating relatively limited long-term impact on overall GDP trajectories. ⁹

In response to the need for greater economic diversification and GDP stability, the state has advanced initiatives aimed at opening the coastline to future trade and commercial activity. This approach has been framed within a broader federal effort to diversify Pacific access points, reduce logistical vulnerabilities, and improve resilience to external trade disruptions.¹⁰ The proposed port development concept in Boca de Chila is not intended to compete directly with established deep-water ports such as Manzanillo or Lázaro Cárdenas, but rather to function as a complementary, long-term option that expands redundancy and regional connectivity.¹⁰

Official federal–state coordination meetings under the Plan de Prosperidad Compartida emphasize sustainable coastal and tourism development, including supporting infrastructure and potential maritime connectivity, rather than the immediate construction of a deep-water commercial cargo port.¹⁰ As such, assessment suggests that near-term growth remains centered on services and tourism, with port-related commercial activity representing a longer-term pathway contingent on future development needs.¹⁰

Nayarit’s GDP is composed of three primary sectors: primary activities (approximately 7.8 percent), including agriculture and fishing; secondary activities (approximately 20.3 percent), dominated by agricultural processing and construction materials; and tertiary activities (approximately 65.7 percent), encompassing tourism, real estate, commerce, and public services.¹¹ Using INEGI’s reported nominal GDP of MXN 218.9 billion in 2023, and applying a staff exchange-rate conversion of 0.0565 USD per MXN, Nayarit’s nominal GDP is estimated at approximately USD $12.3 billion.¹²

Domestic investment constitutes the predominant share of capital formation in the state, accounting for an estimated 85–90 percent of total investment activity in 2025, with foreign direct investment (FDI) playing a complementary role.¹³ Based on available information, staff estimates that total investment activity in Nayarit in 2025 amounted to approximately USD $5.5 billion, of which USD $4.7–5.1 billion was domestically financed and USD $0.4–0.6 billion reflected FDI inflows.¹⁴ This structure is broadly consistent with Nayarit’s service-oriented economic model and reliance on nationally financed tourism, real estate, and public infrastructure projects.¹³¹⁴

II: Microeconomic Analysis (La Peñita de Jaltemba)

La Peñita de Jaltemba is located in northern Nayarit along Federal Highway 200, a coastal corridor that predates the state’s more recent highway expansions and continues to serve as a primary axis of regional connectivity. The town’s geographic position places it between major demand centers—most notably Guadalajara and the Puerto Vallarta metropolitan area—enabling increasing integration into regional tourism, labor, and services markets.

Nayarit’s development trajectory has followed a spatially incremental pattern, characterized by the northward extension of tourism-led and service-oriented growth originating in neighboring Jalisco. This process has progressed sequentially through Puerto Vallarta, Nuevo Nayarit, Bucerías, La Cruz de Huanacaxtle, Punta Mita, Sayulita, and San Pancho, with La Peñita de Jaltemba representing the next stage in this corridor-based expansion. This pattern reflects the diffusion of investment, demand, and infrastructure along established transport routes rather than isolated or exogenous development shocks.

The expansion of this growth corridor has been supported by high-capital investments concentrated around La Peñita, including a joint project with the Marriott Group (Nauka) and development activity associated with the globally established One&Only luxury hotel brand. The town’s urban form further contributes to its attractiveness. Primary roads connecting to the central plaza are laid out in a grid system, in contrast to nearby destinations such as Sayulita, where rapid development across varied elevation has contributed to congestion and pronounced fluctuations in population density during peak travel periods.

In La Peñita, increased investment activity has led to the conversion of private homes and land parcels into development-ready sites. Analysis of municipal building permits, real estate inventories, and local development announcements indicates that approximately 25 to 40 major development projects are underway as of 2025. These include residential condominiums, short-term rental complexes, boutique hotels, mixed-use commercial developments, and new subdivisions. While precise enumeration is constrained by data availability at the local level, the observed project pipeline is broadly consistent with corridor-based urban expansion patterns in northern Nayarit. Eleven condominium developments are currently active, ranging from projects nearing completion to sites undergoing demolition and land clearing as of the end of the fourth quarter.

The scale and composition of development activity have begun to materially affect local factor markets, particularly labor and housing. Construction activity and expanding tourism services have increased demand for both skilled and semi-skilled labor, drawing workers from neighboring municipalities and, in some cases, from larger metropolitan areas such as Mexico City. This has contributed to upward wage pressures in construction trades, property maintenance, hospitality services, and transport-related activities. However, these gains remain uneven and closely tied to project timelines and seasonal tourism cycles, reinforcing employment volatility and underemployment risks outside peak periods. Over time, a more continuous development pipeline may help moderate these fluctuations by supporting steadier population growth and labor demand.

At the same time, rising investment demand has exerted upward pressure on land values and housing costs, as private homes are converted into short-term rentals or redeveloped into higher-density residential and hospitality uses. While this process has expanded the local tax base and stimulated service-sector growth, it has begun to constrain housing affordability in prime areas for resident workers, raising concerns about labor retention and commuting costs. These dynamics suggest that La Peñita is entering a transition phase in which development-led growth increasingly interacts with local capacity constraints, particularly in labor supply and housing availability.

Rising development intensity has also increased demands on local infrastructure systems, most notably water supply, wastewater treatment, transport circulation, and electricity distribution. Although the town’s relatively orderly grid layout provides structural advantages over more organically developed coastal destinations, infrastructure capacity has not expanded at the same pace as private investment activity. Water and sanitation systems represent a critical binding constraint. Higher residential density, the conversion of housing stock into short-term rentals, and the entry of higher-end hospitality developments have raised per-capita water consumption and amplified seasonal peak demand. In the absence of proportional upgrades to water sourcing, storage, and wastewater treatment facilities, these pressures risk reducing service reliability and generating negative externalities, including environmental stress on coastal and nearshore ecosystems. From a growth perspective, such constraints reduce the marginal returns to additional private investment and increase the premium placed on sites with existing and reliable water access.

Transport infrastructure presents a more mixed picture. Federal Highway 200 continues to provide strong regional connectivity and supports La Peñita’s integration into the broader coastal development corridor. However, increased local traffic associated with construction activity, tourism inflows, and service delivery has begun to strain internal road networks during peak periods. While congestion remains less acute than in nearby destinations such as Sayulita or San Pancho, continued development in the absence of coordinated traffic management and parking solutions could erode this comparative advantage over time. To date, these pressures have been partially mitigated through partnerships between municipal authorities and private developers to upgrade local infrastructure, reflecting efforts to sustain development momentum while maintaining service quality.

Electricity and telecommunications infrastructure have, to date, absorbed rising demand more effectively. Nevertheless, increasing loads from higher-density residential projects and hospitality facilities suggest that forward-looking capacity planning will become increasingly important. In aggregate, current infrastructure conditions indicate that La Peñita is approaching a phase in which public investment sequencing—particularly in water, sanitation, and local mobility—will be decisive in determining whether growth remains orderly or becomes constrained by service shortfalls.

III: Legality, Zoning, and Institutional Constraints

Development outcomes in La Peñita de Jaltemba are governed not only by market forces and infrastructure capacity, but also by a multi-layered legal and institutional framework spanning municipal, state, and federal jurisdictions. While zoning and construction permitting are primarily administered by the Municipality of Compostela, land use along the coastline is subject to additional federal regulation under Mexico’s coastal and environmental law.²⁶ As development activity accelerates, the interaction between private investment incentives and these legal constraints plays a decisive role in shaping the scale, form, and sequencing of growth.²⁶

At the municipal level, zoning regulations define allowable land uses, density, building heights, and setbacks. These frameworks were originally designed for low-density residential and small-scale commercial activity and have been placed under increasing strain by demand for higher-density residential, short-term rental, and hospitality projects.²⁷ As a result, development feasibility often depends on zoning classifications at the parcel level and, in some cases, on the ability to obtain zoning modifications or special authorizations.²⁷ From a microeconomic perspective, zoning functions as a scarcity mechanism, raising the value of parcels with clearly defined development rights while increasing transaction costs and uncertainty for projects requiring regulatory adjustment.²⁷

Along the coastline, land use is further constrained by federal law governing the Zona Federal Marítimo Terrestre (ZOFEMAT). Under the Ley General de Bienes Nacionales, the first 20 meters inland from the high-tide line constitute federal public property that cannot be privately owned and must remain accessible to the public (Articles 7, 8, and 119).²⁸ Development within this zone is prohibited for private ownership and strictly limited even for auxiliary or temporary uses.²⁸ Only beyond this federally protected strip may land be privately owned, subject to municipal zoning and environmental regulation. In practice, this legal boundary creates a sharp distinction between public coastal space and privately developable land, significantly influencing project design, density, and valuation.²⁸ Parcels immediately adjacent to, but legally beyond, the ZOFEMAT boundary command substantial price premiums due to the combination of proximity to the shoreline and legally secure ownership.²⁸

Projects near the coastline or environmentally sensitive areas may also be subject to federal environmental review under the Ley General del Equilibrio Ecológico y la Protección al Ambiente (LGEEPA), which requires a Manifestación de Impacto Ambiental (MIA) for developments exceeding defined thresholds.²⁹ Environmental compliance introduces additional fixed costs and timing uncertainty, particularly in coastal contexts where ecosystem sensitivity is higher.²⁹ These requirements tend to favor developers with greater technical and legal capacity, reinforcing segmentation between large, well-capitalized firms and smaller local actors.²⁹

The permitting process itself involves multiple administrative steps, including land-use authorization, construction licenses, infrastructure connection approvals, and, where applicable, environmental clearances. While formally established, the sequencing and duration of these approvals can vary depending on project scale and administrative capacity.³⁰ During periods of rapid development, municipal processing capacity becomes a binding constraint, raising delays and financing costs.³⁰ From an economic standpoint, permitting uncertainty acts as an implicit barrier to entry, shaping market structure and favoring developers capable of absorbing regulatory risk.³⁰

Pre-construction sales (“preventa”) play a central role in financing residential and mixed-use developments in La Peñita de Jaltemba. By securing buyer commitments prior to completion, developers reduce reliance on external financing and transfer part of the project risk to purchasers.³¹ However, preventa arrangements introduce legal risks related to delivery timelines, escrow management, and consumer protection. While such transactions are governed by the Ley Federal de Protección al Consumidor, enforcement and dispute resolution can vary, and delays or project modifications may undermine buyer confidence if not managed transparently.³¹ As development scales, the credibility and standardization of preventa practices become increasingly important for maintaining market stability.³¹

Taken together, zoning regulation, coastal land law, environmental oversight, permitting capacity, and preventa frameworks create a complex regulatory environment that both enables and constrains development in La Peñita de Jaltemba. These legal structures do not prevent investment, but they shape its distribution, timing, and risk profile.³² Uncertainty surrounding zoning adjustments, permitting timelines, and coastal compliance raises transaction costs and land price dispersion, while asymmetries in regulatory navigation capacity favor larger developers.³²

From a broader economic perspective, the primary challenge is not the presence of regulation, but regulatory predictability and institutional capacity. Clear zoning rules, consistent enforcement of coastal protections, transparent permitting processes, and standardized consumer safeguards are essential to aligning private investment incentives with public objectives.³³ As La Peñita transitions from rapid expansion toward a more mature development phase, the effectiveness of these legal and institutional frameworks will play a decisive role in determining whether growth remains orderly, inclusive, and environmentally sustainable.³³ Although grounded in the specific context of La Peñita de Jaltemba, the regulatory dynamics described above reflect challenges commonly faced by secondary coastal destinations experiencing rapid tourism-led development.³³

IV: a look into four separate firms

Within the development sector of Bahía de Banderas and northern Nayarit, several firms illustrate distinct approaches to market entry, capital deployment, and client segmentation.³⁴ Taken together, these enterprises reflect the layered structure of the regional development ecosystem, ranging from locally anchored residential projects to globally branded, capital-intensive hospitality investments.³⁴

Alta Vida: Phased Residential Development and Local Capital Integration

Alta Vida represents a locally anchored residential development model oriented toward North American housing preferences.³⁵ The firm’s flagship project comprises 196 units, complemented by planned recreational amenities, including a nine-hole golf course.³⁵ Development is structured as a multi-phase project with an estimated five-year completion horizon.³⁵

Alta Vida’s business model relies on integration with local construction, materials, and finishing firms, allowing for cost control and responsiveness to local conditions.³⁶ Initial development phases prioritize internal infrastructure, including road networks and community facilities, followed by residential construction.³⁶ Early-stage presales—approximately 34 percent of initial inventory sold within four months—indicate effective demand capture and provide internal financing for subsequent phases.³⁶ This phased approach mitigates capital risk while enabling gradual scale expansion.³⁶

Playa Vida: Brokerage-Led Development and Capital Recycling

Playa Vida operates as a hybrid brokerage–development firm, with a primary client base drawn from U.S. markets, particularly California.³⁷ The firm’s revenue model is diversified across brokerage commissions, property management, and direct development activity.³⁷ Commission structures vary by project, while managed rental properties generate recurring income through short-term leasing, with management fees capturing a fixed share of rental revenue during peak seasons.³⁷

More recently, Playa Vida has expanded into small-scale, internally developed residential projects, employing a capital-recycling model.³⁸ The firm acquires property, secures joint investment partners, completes permitting, and initiates pre-construction sales to finance development.³⁸ Completed units may be retained within the firm’s rental portfolio, creating an integrated sales–management–investment cycle.³⁸ This model emphasizes flexibility and rapid capital turnover rather than scale.³⁸

NAUKA: Brand-Anchored Joint Venture and Asset-Light Strategy

Nauka represents a flagship development within Nayarit’s emerging coastal corridor and operates as a joint venture between local development capital and the Marriott Group, through its Ritz-Carlton Reserve brand.³⁹ The project is characterized by large-scale, low-density land control, enabling the internalization of infrastructure, environmental compliance, and amenity provision.³⁹

Initial capital commitments—estimated at approximately USD 50 million for early development phases—are deployed in a staged manner, concentrating on site preparation and infrastructure provisioning.⁴⁰ Nauka’s operating model reflects Marriott’s asset-light strategy, under which the brand provides branding, operational oversight, and global distribution in exchange for management and performance-based fees, while real estate risk is retained by the development entity.⁴⁰ This structure reduces market-entry risk while leveraging global demand pipelines.⁴⁰

From a regional perspective, Nauka functions as an anchor investment, shaping land valuations and development standards while establishing a first-mover advantage through early regulatory and environmental compliance.⁴¹

Mandarina One&Only: Capital-Intensive Entry and First-Mover Positioning

Mandarina One&Only represents an earlier large-scale investment that materially influenced the development trajectory of Nayarit’s northern coastal corridor. Operating under the One&Only brand, part of Kerzner International, the project follows a vertically integrated development model in which the developer retained control over land acquisition, infrastructure provisioning, and long-term asset strategy.⁴²

Significant upfront capital investment in infrastructure and regulatory compliance created high fixed costs and raised entry barriers for subsequent competitors.⁴³ Mandarina’s operating model emphasizes limited capacity and high revenue per unit, prioritizing pricing power over volume expansion.⁴³ The integration of residential components alongside hospitality operations diversified revenue streams and accelerated capital recovery.⁴³

At the regional level, Mandarina functioned as a market-signaling investment, demonstrating the feasibility of ultra-luxury, low-density development within Nayarit’s regulatory and environmental constraints and shaping expectations for later entrants.⁴⁴

V: Positioning Through Cross-Channel Investment and Collaboration

As La Peñita de Jaltemba transitions from rapid, development-led expansion toward greater structural maturity, its long-term economic positioning is increasingly shaped by cross-channel investment flows and interregional collaboration.⁴⁵ Rather than functioning as an isolated local market, the town has become embedded within a broader coastal economic system linking northern Nayarit with southern Jalisco and the Puerto Vallarta metropolitan area.⁴⁵ This integration operates through interconnected channels of capital, labor, services, and institutions, influencing both growth dynamics and resilience.⁴⁵

Private investment in La Peñita reflects spillovers from more mature coastal destinations to the south, where rising land prices, congestion, and regulatory saturation have redirected developer interest toward adjacent, lower-density markets.⁴⁶ La Peñita’s location along Federal Highway 200 and its proximity to established tourism hubs enable it to absorb incremental demand while benefiting from existing branding, financing networks, and market recognition.⁴⁶ From a microeconomic perspective, this spillover dynamic lowers entry barriers and accelerates project viability, while simultaneously increasing exposure to shifts in investor sentiment and financing conditions in upstream markets.⁴⁶

Demand for residential, hospitality, and short-term rental products is similarly integrated with external markets, particularly Guadalajara and the broader Jalisco metropolitan region.⁴⁷ These demand centers provide a steady flow of domestic visitors and second-home buyers who view La Peñita as an extension of the coastal leisure corridor rather than a standalone destination.⁴⁷ While this integration supports baseline demand, it also links local outcomes to broader macroeconomic conditions affecting household income, credit availability, and travel costs.⁴⁷

Labor market integration constitutes a further channel of cross-regional interaction. Construction, hospitality, and property services increasingly rely on workers from neighboring municipalities and major metropolitan areas.⁴⁸ This mobility supports short-term growth despite local housing constraints but introduces medium-term risks related to labor retention, commuting costs, and service quality.⁴⁸ Without coordinated regional planning—particularly in housing supply, transport connectivity, and skills development—these dynamics may constrain productivity gains as development matures.⁴⁸

Service integration reinforces La Peñita’s position within the corridor. Higher-order services such as design, legal advisory, finance, and specialized construction are frequently sourced from regional hubs, reducing fixed costs for local projects but limiting local value capture.⁴⁹ Over time, the development of localized service capacity could enhance income retention and stabilize economic activity, particularly as construction cycles moderate.⁴⁹

Institutional collaboration has emerged as a partial response to shared infrastructure and service constraints. Partnerships between municipal authorities, state agencies, and private developers have facilitated incremental upgrades in water, sanitation, and mobility systems.⁵⁰ From an economic standpoint, such collaboration helps internalize spillover effects that individual municipalities may struggle to address independently, improving the marginal returns to private investment.⁵⁰

Within the broader coastal growth hierarchy, La Peñita functions as a secondary growth node, complementing rather than competing with established destinations.⁵¹ Its comparative advantage lies not in scale, but in connectivity and coordination—absorbing incremental demand while maintaining relatively lower congestion and a more orderly urban form.⁵¹ Cross-channel integration thus serves as both a growth mechanism and a risk-mitigation strategy, provided governance and regulatory coherence are maintained.⁵¹

VI. Investing Capital: Foreign Ownership Structures and Intergenerational Transfers

Foreign capital has played an increasingly important role in Nayarit’s coastal development, particularly in residential and hospitality real estate.⁵² Accordingly, the legal framework governing foreign land ownership is relevant for assessing the durability of capital formation, the continuity of property rights, and the long-term implications for land and housing markets in coastal municipalities such as La Peñita de Jaltemba.⁵²

Article 27 of the Mexican Constitution establishes that land and waters within national territory are vested in the nation. Under this framework, foreign individuals are prohibited from direct personal ownership of land within the restricted zone, defined as 50 kilometers from the coastline and 100 kilometers from international borders.⁵³ As much of Nayarit’s coastal territory lies within this zone, foreign participation in coastal real estate is conducted through legally established ownership structures rather than direct fee-simple title held in an individual’s name.⁵³

Importantly, these restrictions do not preclude ownership in an economic or legal sense. Mexican law provides mechanisms through which foreign nationals acquire recognized property rights, backed by registered deeds and enforceable under Mexican law.⁵⁴ The primary mechanism through which foreign individuals acquire residential property in the restricted zone is the fideicomiso, or bank trust.⁵⁴ Under this arrangement, a Mexican financial institution holds legal title to the property as trustee, while the foreign investor is designated as the beneficial owner of the asset.⁵⁴

The property is recorded in the Public Registry of Property, and a formal deed (escritura) exists for the asset.⁵⁵ While the trustee appears as the titleholder in a technical sense, the beneficiary holds all substantive ownership rights, including exclusive possession and use of the property, the right to lease or sell the property, the right to encumber the asset, the right to improve or redevelop the property (subject to zoning and permitting requirements), and the right to designate successors and heirs.⁵⁵

From a legal and economic perspective, this structure constitutes recognized ownership, with the fideicomiso serving as the constitutional vehicle through which title is held and enforced.⁵⁶ Fideicomisos are typically established for renewable 50-year terms, ensuring continuity of ownership across time.⁵⁶ Although fideicomisos are sometimes informally described as “100-year leases,” they are not leases; rather, they are renewable trust structures with no statutory limit on renewals.⁵⁶

A defining feature of the fideicomiso structure is its capacity to support intergenerational transfer of ownership rights.⁵⁷ Once property is acquired legally, beneficiaries may designate heirs within the trust documentation.⁵⁷ Upon succession, beneficial ownership transfers to the designated successor(s) without liquidation of the asset or loss of title registration.⁵⁷ In practice, this allows property to remain within a family across multiple generations, provided that trust renewals and notarial requirements are maintained.⁵⁷ The continuity of registered title and enforceable ownership rights ensures that foreign-held property functions as a long-term asset, rather than a temporary concession.⁵⁷

Foreign investors may alternatively acquire property through Mexican legal entities, most commonly corporations.⁵⁸ In this case, the corporation holds direct legal title to the land, recorded by deed in the Public Registry of Property in the same manner as domestic ownership.⁵⁸ Foreign investors then hold equity interests in the entity rather than in the property itself.⁵⁸ Intergenerational transfer occurs through inheritance or transfer of shares, while the underlying land title remains unchanged.⁵⁸ This structure is commonly used for commercial, hospitality, and multi-unit residential developments and offers greater flexibility for financing and portfolio management.⁵⁸

Both fideicomiso and corporate ownership structures are subject to federal oversight, including authorization by the Secretaría de Relaciones Exteriores, notarial certification, and registration in the Public Registry of Property.⁵⁹ Developments remain subject to municipal zoning, state planning regulations, environmental law, and federal coastal land provisions, including ZOFEMAT, where applicable.⁵⁹ Provided these requirements are met, foreign-owned property enjoys full legal certainty, with ownership rights enforceable under Mexican law and protected in the same registries and courts that govern domestic property rights.⁵⁹

From an economic standpoint, the legal recognition of foreign ownership—combined with the ability to hold registered title and transfer property across generations—transforms international real estate investment from short-term speculation into durable capital formation.⁶⁰ Longer ownership horizons support higher construction quality, sustained reinvestment, and deeper integration into local service economies.⁶⁰ At the same time, increased foreign participation can intensify competition for land and housing, reinforcing the importance of complementary policies related to zoning, housing supply, and infrastructure capacity.⁶⁰

Taken together, the macroeconomic, microeconomic, legal, and firm-level analyses demonstrate that development outcomes in Nayarit are determined less by the absolute scale of capital deployed than by the strategic positioning of that capital within a constrained and evolving regional system. At the macro level, public infrastructure investment and regional integration with Jalisco have expanded access and demand but have not eliminated structural bottlenecks. At the micro level, La Peñita de Jaltemba illustrates how localized constraints in labor supply, housing affordability, and water and transport capacity shape the marginal returns to additional investment. Legal and institutional frameworks—including zoning regulation, coastal land protections, environmental permitting, and pre-construction financing practices—further mediate who can build, where, and at what pace. Within this environment, firm-level outcomes diverge sharply: developers that successfully align location, regulatory navigation, branding, and phased execution achieve durable advantages, while scale alone offers limited protection against institutional and infrastructural constraints. The evidence, therefore, suggests that market dominance in Nayarit emerges from the ability to position capital across infrastructure readiness, legal certainty, and demand integration, rather than from size or capital intensity in isolation.

Numbered Endnotes

· Author calculations based on publicly announced federal and state infrastructure programs in Nayarit over the past decade, including priority transport, highway, and airport projects reported by the Secretaría de Infraestructura, Comunicaciones y Transportes (SICT), converted to U.S. dollars using period-average exchange rates.

· The estimate that approximately 8–13 percent of decade-long public infrastructure investment was executed in 2025 reflects author judgment, consistent with the back-loaded execution profile of large multi-year transport and airport projects.

· Nominal GDP figures for Jalisco are reported by the Instituto Nacional de Estadística y Geografía (INEGI), Producto Interno Bruto por Entidad Federativa. U.S. dollar equivalents reflect author conversions using 2023 annual average exchange rates from Banco de México.

· Estimates of middle-income and upper-middle-income population shares in the Guadalajara metropolitan area reflect author calculations based on household income survey distributions from INEGI’s Encuesta Nacional de Ingresos y Gastos de los Hogares (ENIGH). These classifications are not official INEGI income classes.

· Tourism’s contribution to Jalisco’s GDP is based on state tourism satellite accounts. Estimates of Puerto Vallarta’s share reflect author calculations combining tourism GDP shares and destination-level activity reported by state tourism authorities.

· Grupo Aeroportuario Turístico Mexicano (GATM) reports that completed modernization works at Tepic–Riviera Nayarit International Airport—including runway rehabilitation, new control tower, terminal upgrades, aprons, and access roads—were executed with an investment exceeding USD 146 million, corresponding to completed or initial project phases.

· Official project documentation reports a broader Tepic airport expansion program of approximately MXN 4.1 billion (USD 223–239 million), implemented under a public–private investment model over the 2023–27 period.

· The new Terminal 2 at Puerto Vallarta International Airport represents an investment of approximately MXN 9.2 billion (USD ~490 million) and is being executed by Grupo Aeroportuario del Pacífico (GAP). Public disclosures indicate construction progress of approximately 54 percent as of 2025, with completion targeted for mid-2027.

· Tourism demand trends are based on Secretaría de Turismo (SECTUR) DataTur statistics, using hotel arrivals aggregated from monthly to annual totals.

· Federal–state coordination meetings in Boca de Chila under the Plan de Prosperidad Compartida emphasize sustainable coastal and tourism development. Interpretations regarding future trade diversification reflect author assessment based on official public statements rather than confirmed port construction plans.

· Sectoral shares of Nayarit’s GDP are based on INEGI’s Producto Interno Bruto por Entidad Federativa (2023), reporting primary activities at approximately 7.8 percent, secondary activities at 20.3 percent, and tertiary activities at 65.7 percent.

· Nayarit’s nominal GDP of MXN 218.9 billion in 2023 (INEGI) is converted to U.S. dollars using an author exchange-rate assumption of 0.0565 USD per MXN, consistent with annual market averages.

· Estimates that domestic investment accounts for 85–90 percent of total investment activity, with foreign direct investment (FDI) comprising 10–15 percent, are author calculations derived from public capital expenditure data and state-level FDI inflows reported by the Secretaría de Economía.

· Total investment activity in Nayarit in 2025 (approximately USD 5.5 billion) reflects author aggregation of public infrastructure spending and announced private development projects.

· Secretaría de Infraestructura, Comunicaciones y Transportes (SICT). Federal Highway 200 transport corridor documentation.

· Author assessment based on observed tourism flows, labor mobility, and travel-time integration between Guadalajara, Puerto Vallarta, and northern Nayarit.

· Author interpretation of regional development sequencing using historical tourism expansion patterns across Jalisco and Nayarit.

· Marriott International (Ritz-Carlton Reserve) and Kerzner International (One&Only) project disclosures and public announcements.

· Municipal urban development plans and comparative spatial analysis of coastal town layouts (Sayulita versus La Peñita).

· Municipio de Compostela building permit records; local real estate inventories; author aggregation of announced development projects.

· Author assessment based on construction activity, ENOE labor market indicators, and observed inter-municipal migration patterns.

· Author interpretation based on housing price trends, short-term rental conversion rates, and observed affordability pressures.

· Municipal infrastructure reports and author assessment of water and sanitation capacity constraints.

· Secretaría de Infraestructura, Comunicaciones y Transportes (SICT) traffic counts and author observation of congestion trends along Highway 200 and local road networks.

· Comisión Federal de Electricidad (CFE) service coverage data and author assessment of electricity and telecommunications demand absorption.

· Municipio de Compostela zoning authority and federal–municipal regulatory interaction governing construction permitting.

· Programa Municipal de Desarrollo Urbano de Compostela; author interpretation of zoning classifications and density constraints.

· Ley General de Bienes Nacionales, Articles 7, 8, and 119; Secretaría de Medio Ambiente y Recursos Naturales (SEMARNAT) guidance on the Zona Federal Marítimo Terrestre (ZOFEMAT).

· Ley General del Equilibrio Ecológico y la Protección al Ambiente (LGEEPA); SEMARNAT environmental impact assessment (MIA) procedures.

· Municipal permitting procedures; author assessment of administrative capacity constraints during peak development cycles.

· Ley Federal de Protección al Consumidor; author interpretation of pre-construction sales (preventa) practices.

· Author synthesis of zoning, coastal land, environmental, and permitting frameworks affecting land valuation and investment risk.

· Author assessment consistent with IMF analyses of regulatory predictability and institutional capacity in subnational development contexts.

· Author synthesis of firm-level differentiation and development strategies in Bahía de Banderas and northern Nayarit.

· Alta Vida development materials and municipal filings confirming a 196-unit project configuration.

· Author assessment based on presale disclosures, phased development structures, and local supply-chain integration.

· Playa Vida brokerage disclosures and author assessment of brokerage-led development models.

· Author interpretation of capital-recycling development models using pre-construction sales and rental portfolio integration.

· Marriott International. Ritz-Carlton Reserve project disclosures; NAUKA joint-venture announcements.

· Author estimate based on public project disclosures and phased capital deployment in early NAUKA development stages.

· Author assessment of first-mover advantage and regulatory positioning in emerging coastal zones.

· Kerzner International. One&Only Mandarina project materials.

· Author interpretation of capital intensity, revenue-per-unit strategies, and mixed-use risk diversification.

· Author assessment of market-signaling effects following Mandarina One&Only’s entry.

· Author synthesis of cross-channel investment and regional integration dynamics linking northern Nayarit, southern Jalisco, and Puerto Vallarta.

· Author assessment based on land-price differentials, congestion, and development spillovers along the Pacific coastal corridor.

· Author interpretation of demand integration using tourism flows, second-home ownership patterns, and household income linkages.

· Author assessment based on ENOE labor mobility indicators and construction employment patterns.

· Author interpretation of service outsourcing and value-chain integration in emerging coastal development markets.

· Author assessment of public–private coordination mechanisms for incremental infrastructure upgrades.

· Author synthesis consistent with IMF analyses of secondary growth nodes and corridor-based development.

· Author assessment of foreign capital participation in residential and hospitality real estate markets in coastal Nayarit.

· Constitución Política de los Estados Unidos Mexicanos, Article 27; Ley de Inversión Extranjera.

· Secretaría de Relaciones Exteriores (SRE) guidance on fideicomisos and foreign ownership in the restricted zone.

· Registro Público de la Propiedad (Nayarit) procedures governing registration and enforceability of escrituras.

· Author interpretation of fideicomiso renewal provisions and tenure security under Mexican law.

· Author assessment of intergenerational transfer mechanisms within fideicomiso structures.

· Ley General de Sociedades Mercantiles; author interpretation of corporate ownership and share-transfer mechanisms.

· Secretaría de Relaciones Exteriores; municipal and state regulatory frameworks; Ley General de Bienes Nacionales (ZOFEMAT).

· Author synthesis consistent with IMF analyses of property rights, investment horizons, and durable capital formation.

References

(Place this section immediately after Notes. Do not number entries.)

Banco de México. Exchange Rate Statistics (Annual Averages).

Comisión Federal de Electricidad (CFE). Service Coverage and Capacity Reports.

Gobierno de México. Constitución Política de los Estados Unidos Mexicanos.

Gobierno de México. Ley de Inversión Extranjera.

Gobierno de México. Ley General de Bienes Nacionales.

Gobierno de México. Ley General del Equilibrio Ecológico y la Protección al Ambiente (LGEEPA).

Gobierno de México. Ley Federal de Protección al Consumidor.

Gobierno de México. Ley General de Sociedades Mercantiles.

Instituto Nacional de Estadística y Geografía (INEGI). Producto Interno Bruto por Entidad Federativa.

Instituto Nacional de Estadística y Geografía (INEGI). Encuesta Nacional de Ingresos y Gastos de los Hogares (ENIGH).

Instituto Nacional de Estadística y Geografía (INEGI). Encuesta Nacional de Ocupación y Empleo (ENOE).

Secretaría de Economía. Registro Nacional de Inversiones Extranjeras.

Secretaría de Infraestructura, Comunicaciones y Transportes (SICT). Federal Transport and Highway Reports.

Secretaría de Medio Ambiente y Recursos Naturales (SEMARNAT). Environmental Impact Assessment Guidelines.

Secretaría de Turismo (SECTUR). DataTur Tourism Statistics.

Grupo Aeroportuario del Pacífico (GAP). Investor and Project Disclosures.

Grupo Aeroportuario Turístico Mexicano (GATM). Project Announcements and Press Releases.

Marriott International. Ritz-Carlton Reserve Project Materials.

Kerzner International. One&Only Mandarina Development Materials.

forbes top travel guide 2026

Forbes Travel Guide’s focus on Nayarit reflects the region’s rise as a refined, experience-driven luxury destination. With low-density coastal development, globally recognized hospitality brands, and a strong commitment to sustainability and service excellence, Nayarit offers travelers an alternative to traditional resort markets—one defined by authenticity, discretion, and long-term destination integrity.

Forbes Travel Guide’s recognition of Nayarit reflects the destination’s emergence as one of Mexico’s most compelling luxury and experiential travel regions. The state’s Pacific coastline has undergone a measured transformation, balancing high-end hospitality development with preserved natural landscapes, cultural authenticity, and an increasingly sophisticated service ecosystem.

Unlike more saturated resort markets, Nayarit offers a differentiated proposition: low-density coastal development, world-class branded hospitality, and seamless access to diverse experiences ranging from secluded beaches and rainforest environments to culinary, wellness, and cultural offerings. This combination aligns closely with Forbes Travel Guide’s emphasis on destinations that deliver both exceptional service standards and a strong sense of place.

Recent investments in luxury resorts, branded residences, and supporting infrastructure have elevated the region’s global profile while maintaining environmental and spatial restraint. Developments such as ultra-luxury resorts, boutique coastal communities, and thoughtfully planned residential projects illustrate a commitment to quality over scale—an approach that resonates with Forbes Travel Guide’s focus on refinement, personalization, and long-term destination integrity.

Additionally, Nayarit’s growing accessibility through improved air connectivity and transportation infrastructure has positioned the region as both exclusive and attainable for international travelers seeking elevated experiences beyond traditional mass-tourism destinations. This accessibility, combined with a strong emphasis on sustainability, service excellence, and experiential travel, has contributed to Nayarit’s inclusion among destinations to watch.

In highlighting Nayarit, Forbes Travel Guide underscores a broader shift in luxury travel preferences toward destinations that offer authenticity, discretion, and depth, rather than scale alone. Nayarit’s evolution reflects this trend—establishing the region as a benchmark for next-generation luxury travel along Mexico’s Pacific coast.

Resident a look at Nuaka

Anchored by world-class hospitality and complemented by a carefully limited residential offering, Nauka reflects the future of Riviera Nayarit—one defined by quality over quantity, global sophistication paired with local identity, and a deliberate pace that allows both people and place to thrive. As infrastructure and connectivity across the region continue to advance, Nauka stands positioned not only as a premier destination but as a benchmark for how coastal luxury can evolve responsibly along Mexico’s Pacific coast.

Nestled along one of Mexico’s most pristine and dramatic stretches of coastline, Nauka represents a transformative vision for luxury living and travel on the Riviera Nayarit. Spanning nearly 920 acres of unspoiled landscape where volcanic cliffs, mangrove estuaries, evergreen jungle, and golden Pacific beaches converge, Nauka is designed not merely as a destination, but as a next-generation sanctuary that harmonizes refined modern comforts with deep respect for nature and cultural heritage. Anchored by world-class hospitality and complemented by a carefully limited residential offering, Nauka reflects the future of Riviera Nayarit—one defined by quality over quantity, global sophistication paired with local identity, and a deliberate pace that allows both people and place to thrive. As infrastructure and connectivity across the region continue to advance, Nauka stands positioned not only as a premier destination but as a benchmark for how coastal luxury can evolve responsibly along Mexico’s Pacific coast.